Buying your first home is exciting, but it can also feel like you’re stepping into a whole new world of real estate lingo and financial decisions. That’s why having first-time home buyer mortgage tips at your fingertips is crucial. Since most first-time buyers rely on financing, understanding how mortgages work is key to making smart decisions.

Buying your first home is exciting, but it can also feel like you’re stepping into a whole new world of real estate lingo and financial decisions. That’s why having first-time home buyer mortgage tips at your fingertips is crucial. Since most first-time buyers rely on financing, understanding how mortgages work is key to making smart decisions.

The good news? With the right guidance and a bit of homework, you can avoid common pitfalls and set yourself up for success. Let’s dive into some essential mortgage tips to help you navigate the process with confidence.

“I’m passionate about helping first-time home buyers navigate one of the biggest investments of their lives. With years of experience, I simplify the process, break down the financial details, and add a bit of humor along the way. From budgeting to finding the right loan, my goal is to empower buyers to make smart, confident decisions for a happy future.” -Kevin Wood (Realtor, Author, SRES, SFR, IMSD)

Understand Your Financial Picture

Before you start house hunting, it’s crucial to get a clear understanding of your financial standing. Just because a lender says you can afford a higher mortgage payment doesn’t mean you should stretch your budget to the max.

Consider these factors:

Your current rent vs. potential mortgage payment

Ongoing expenses like vacations, hobbies, and future purchases

Homeownership costs such as maintenance, lawn care, and repairs

Take the time to review your monthly budget to ensure you’re comfortable with your new financial commitments.

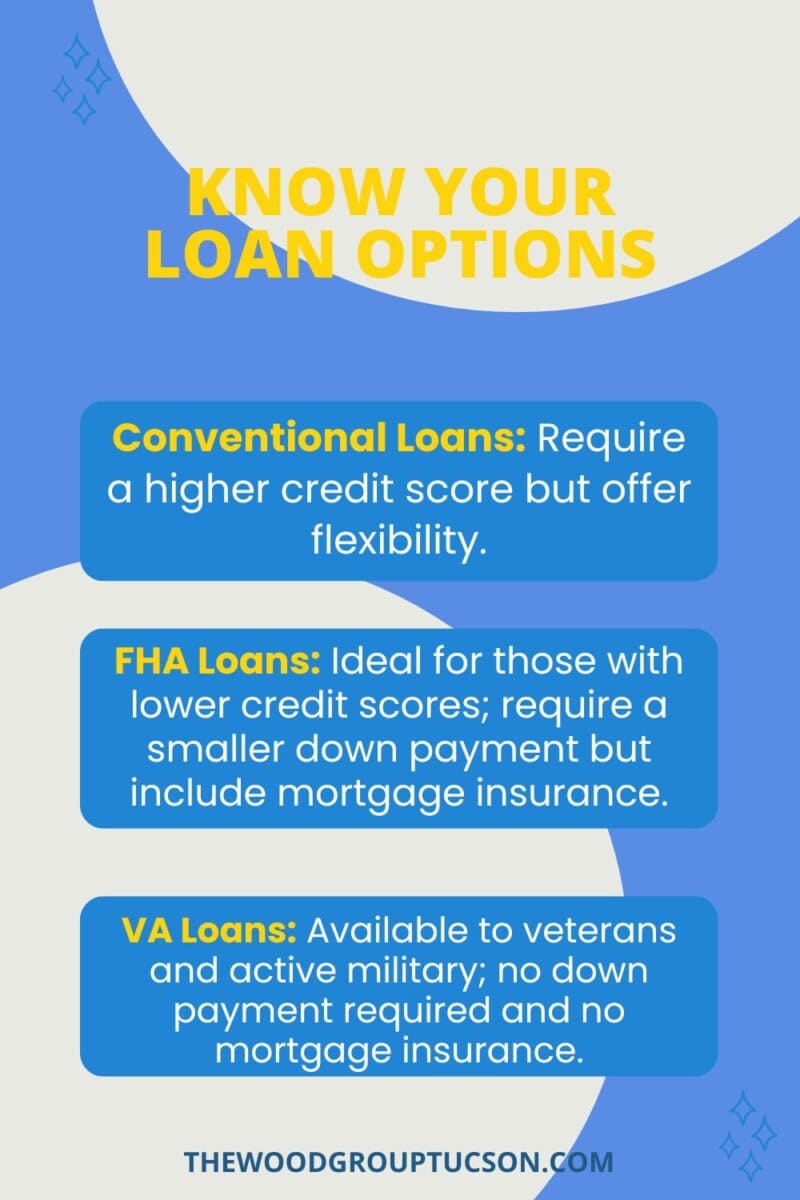

There are several types of mortgages to consider:

There are several types of mortgages to consider:

Conventional Loans: Require a higher credit score but offer flexibility.

FHA Loans: Ideal for those with lower credit scores; require a smaller down payment but include mortgage insurance.

VA Loans: Available to veterans and active military; no down payment required and no mortgage insurance.

Your mortgage lender should walk you through the pros and cons of each option to find the best fit for your situation.

Understand Closing Costs

Closing costs typically range from 3% to 6% of the loan amount and include fees such as:

Loan origination

Appraisal and inspection

Title searches

Attorney fees

Knowing these costs upfront can prevent any last-minute surprises at the closing table.

I’m Kevin Wood, a trusted professional in residential real estate who has served southern Arizona and the surrounding areas since 2005. My knowledge and experience covers a wide range of topics including general real estate, mortgages, financing, seniors, moving, and home improvement.

I’m Kevin Wood, a trusted professional in residential real estate who has served southern Arizona and the surrounding areas since 2005. My knowledge and experience covers a wide range of topics including general real estate, mortgages, financing, seniors, moving, and home improvement.

I can be reached at [email protected] or by phone at 520-260-3123. For the past 19+ years, I’ve helped over 600 families move in and out of southern Arizona and constantly rank among the top 10% of realtors nationwide for performance and client satisfaction.

Are you planning a move? I’m passionate about real estate and enjoy sharing my knowledge and skills in marketing.

I serve people with real estate needs in the following areas of southern Arizona: Tucson, Vail, Corona de Tucson, Sahuarita, Green Valley, Oro Valley, Marana, Picture Rocks, Catalina, Saddlebrooke, Benson, Tanque Verde, Three Points, and Red Rock.